यह India के निवेशकों के बीच सबसे ज़्यादा debate होने वाला सवाल है। एक तरफ ETF है — passive, cheap, transparent। दूसरी तरफ Active Mutual Fund — जिसमें एक expert fund manager आपके पैसे को manage करता है।

दोनों के supporters अपनी-अपनी बात पर अड़े हैं। लेकिन numbers — और खासकर 15 साल का compound effect — इस debate का एक clear जवाब देते हैं।

Expense Ratio — यही असली फर्क है

ETF और Active Mutual Fund के बीच सबसे fundamental difference है expense ratio।

ETF सिर्फ index को copy करता है। कोई research team नहीं, कोई star fund manager नहीं, कोई complex trading नहीं। इसलिए cost बेहद कम होती है। Nifty 50 ETF का expense ratio 0.02% से 0.05% है।

Active Mutual Fund में fund manager, research analysts, trading desk — पूरी टीम होती है। यह cost investors से ली जाती है। Direct plan में 0.5% से 1.5%, Regular plan में 1.5% से 2.5% तक expense ratio होता है।

यह छोटा सा percentage difference 15-20 साल में कितना बड़ा बन जाता है — यही इस article का सबसे important insight है।

Expense Ratio का Compound Effect — The Silent Return Killer

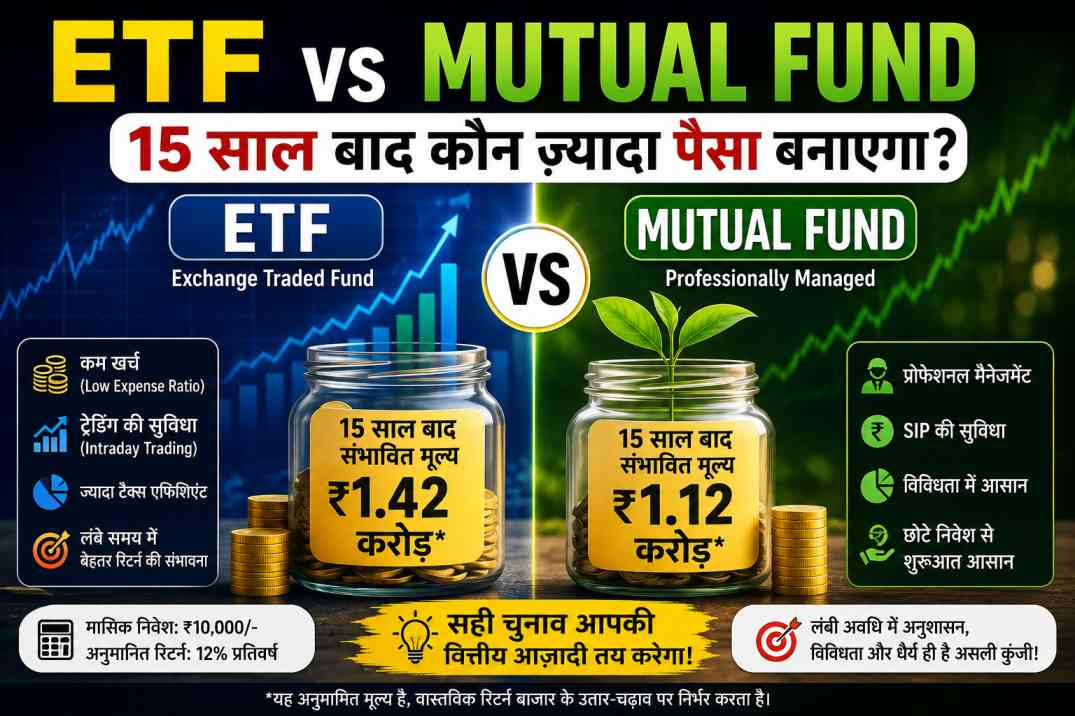

₹10,000 मासिक SIP, 14% gross return, 15 साल:

| Expense Ratio | Net Return | 15 साल का Corpus |

|---|---|---|

| 0.02% (ETF) | 13.98% | ₹51.8 लाख |

| 0.05% (ETF) | 13.95% | ₹51.7 लाख |

| 0.10% (Index Fund) | 13.90% | ₹51.5 लाख |

| 0.50% | 13.50% | ₹50.3 लाख |

| 1.00% | 13.00% | ₹48.6 लाख |

| 1.50% (Active Direct) | 12.50% | ₹46.9 लाख |

| 2.00% (Active Regular) | 12.00% | ₹45.3 लाख |

| 2.50% (Active Regular) | 11.50% | ₹43.8 लाख |

ETF (0.05%) और Active Regular Fund (2.0%) का corpus difference है ₹6.4 लाख — यानी 14% ज़्यादा corpus। और यह सिर्फ expense ratio का फर्क है, fund performance नहीं।

वह ₹6.4 लाख किसी ने आपको दिया नहीं था, आपसे धीरे-धीरे fees के रूप में ले लिया गया था। Compound interest के ज़रिए।

ETF vs Active Fund — पूरी तुलना

| पहलू | ETF | Active Mutual Fund |

|---|---|---|

| Expense ratio | 0.02–0.05% | 0.5–2.5% |

| Fund manager | नहीं — index track | हाँ — active management |

| Transparency | Daily holdings | Monthly disclosure |

| Liquidity | Real-time trade | Day-end NAV |

| Demat account | ज़रूरी | ज़रूरी नहीं |

| SIP automation | Manual / broker | Easy auto-debit |

| Tax | LTCG 12.5% | LTCG 12.5% (same) |

| Alpha potential | नहीं — index return | हाँ — manager skill पर |

| Tracking error | थोड़ा | N/A |

| Minimum investment | 1 unit (~₹100-300) | ₹100-500 |

Tax — दोनों बराबर हैं

यहाँ एक common misconception clear करना ज़रूरी है। कुछ लोग सोचते हैं ETF पर कम tax लगता है। यह गलत है।

India में Equity ETF और Equity Mutual Fund दोनों पर same tax treatment है। 1 साल से ज़्यादा hold करने पर LTCG लगता है। ₹1.25 लाख सालाना profit tax-free है। उसके ऊपर 12.5% LTCG।

Tax के मामले में दोनों exactly equal हैं। Corpus का अंतर सिर्फ expense ratio की वजह से है।

SPIVA India Report — Data जो सब कुछ कह देता है

S&P Indices Versus Active (SPIVA) India Report हर साल active vs passive performance का data publish करती है। 2024 की report के निष्कर्ष चौंकाने वाले हैं।

Large Cap category में 10 साल की अवधि में 80%+ active funds ने अपने Nifty 50 benchmark को underperform किया। यानी 100 में से 80 fund managers, एक index ETF से भी कम return दे पाए।

Mid Cap में यह number थोड़ा बेहतर है — 60-65% funds underperform करते हैं। Small Cap में fund managers ज़्यादा value add करते हैं क्योंकि यहाँ information asymmetry होती है।

Active Fund कब जीत सकता है?

अब fair picture के लिए — कुछ situations में active fund ETF से बेहतर हो सकता है।

जब Fund Manager Consistent Alpha देता हो

अगर कोई fund manager लगातार index को 2-3% ज़्यादा return दे रहा है, तो expense ratio का नुकसान cover हो जाता है। India में कुछ mid/small cap fund managers ने यह prove किया है।

Mirae Asset Large Cap, SBI Small Cap, Parag Parikh Flexicap जैसे funds ने लंबे समय में index से consistently ज़्यादा return दिया है।

Small और Mid Cap में

Large cap में information efficient है — सब analysts एक ही stocks follow करते हैं। लेकिन mid और small cap में fund managers को genuine research edge मिल सकता है। यहाँ active management value add कर सकती है।

Direct Plan में

Direct plan में expense ratio 0.5-1.0% तक आ जाता है — जो active fund को ETF के ज़्यादा comparable बनाता है। Regular plan (जो distributor के ज़रिए लिया जाता है) में 1.5-2.5% expense ratio हमेशा avoid करना चाहिए।

Index Fund vs ETF — क्या दोनों same हैं?

यह भी एक common confusion है।

Index Fund और ETF दोनों same index track करते हैं — जैसे Nifty 50, लेकिन structure अलग है।

ETF stock exchange पर real-time trade होता है। Index Fund mutual fund की तरह day-end NAV पर buy/sell होता है।

Expense ratio में Index Fund ETF से थोड़ा ज़्यादा होता है (0.10% vs 0.05%) लेकिन यह difference negligible है।

SIP के लिए Index Fund ज़्यादा convenient है — auto-debit आसान है और Demat की ज़रूरत नहीं। Long term investors के लिए दोनों practically same corpus देते हैं।

Core-Satellite Strategy — दोनों का Best Combination

Actual बेस्ट strategy यह है कि ETF/Index Fund और Active Fund को compete नहीं, complement करें।

Core portfolio (70-80%) में Nifty 50 ETF या Index Fund रखें। यह stable, low-cost, diversified base है। Index की growth capture होती है।

Satellite portfolio (20-30%) में proven active funds रखें — particularly mid/small cap जहाँ alpha की possibility है। अगर fund manager outperform करे तो extra return मिलता है। अगर underperform करे तो core portfolio को hold करता है।

यह strategy internationally “lazy portfolio with alpha kickers” के नाम से जानी जाती है।

Regular Plan vs Direct Plan — एक ज़रूरी Warning

अगर आप Active Mutual Fund चुनते हैं, तो Regular Plan से ज़रूर बचें।

Regular Plan में distributor commission होती है जो expense ratio में जुड़ती है। यह extra 0.5-1.0% हर साल आपके corpus को drain करती है।

हमेशा Direct Plan चुनें — AMC website, MFCentral, Zerodha Coin, या Groww पर directly invest करें।

₹10,000 SIP, 15 साल में Regular vs Direct Plan का फर्क: Regular Plan (2.0% expense): ₹45.3 लाख। Direct Plan (1.0% expense): ₹48.6 लाख। फर्क: ₹3.3 लाख।

ETF में कैसे और कहाँ Invest करें?

Zerodha Kite / Coin

Zerodha पर Demat account खुलवाएं (free है)। Kite app पर NIFTYBEES, JUNIORBEES, या UTI NIFTY50 search करें और units खरीदें। Coin platform पर Index Funds में SIP भी लगा सकते हैं।

Groww

Groww पर ETF और Index Fund दोनों एक ही platform पर invest होते हैं। ETF में “one-time” purchase और Index Fund में SIP दोनों options हैं।

Direct AMC Websites

Nippon India, Mirae Asset, UTI, HDFC AMC की websites पर directly Index Fund SIP शुरू कर सकते हैं। Demat की ज़रूरत नहीं, expense ratio minimum।

निष्कर्ष — Numbers का Final Verdict

15 साल के data का निष्कर्ष बिल्कुल clear है।

Expense ratio ETF के favor में है — यह mathematical certainty है। जो हर साल कम fee लेता है, वह compound interest के ज़रिए ज़्यादा corpus बनाता है।

लेकिन अगर कोई active fund manager consistently 2%+ alpha generate करता है, तो वह expense ratio के बाद भी ETF को beat कर सकता है।

India में 80% active large cap funds ने index को underperform किया है। लेकिन जो 20% outperform करते हैं, उनमें से कुछ genuinely talented managers हैं।

Practical answer यह है: ETF को core रखें, proven active funds को satellite। Expense ratio minimize करें। Regular Plan से हमेशा बचें। And above all — जो भी चुनें, SIP discipline बनाए रखें।

“The greatest enemy of a good plan is the dream of a perfect plan.” — Carl von Clausewitz. ETF perfect है या Active Fund — यह debate करने में जितना समय लगाएं, उससे आधे समय में SIP शुरू कर दें।

Disclaimer: यह article केवल educational purpose के लिए है। Returns historical assumptions पर आधारित हैं। Expense ratios समय के साथ बदलती हैं। Mutual Fund और ETF investments market risk के अधीन हैं। निवेश से पहले SEBI registered financial advisor से सलाह लें।

Read Also: भारत में International ETF में Invest करना सही है?

Read Also: Market Crash में कौन से ETFs सबसे कम गिरते हैं?

Read Also: Nifty 500 ETF: क्या यह Future का Best Investment है?

नमस्कार दोस्तों, मेरा नाम वरुण सिंह है, मैं अपने खाली समय में Youtube Channel पर फाइनेंस संबंधी वीडियो अपलोड करता हूं साथ ही ब्लॉगिंग भी कर रहा हूं। हमारी कोशिश है की हम अपने पाठकों के लिए फाइनेंस सम्बंधित विषयों पर उच्च गुणवत्ता से युक्त आर्टिकल प्रकाशित करें।